The Impact of ESG Disclosure on Organizational Performance: Evidence from Emerging Markets

DOI:

https://doi.org/10.31313/rygd4404Keywords:

ESG disclosure, organizational performance, emerging markets, stakeholder theory, institutional theory, sustainability governanceAbstract

Background: Environmental, Social, and Governance (ESG) disclosure has become increasingly important in corporate governance and global capital markets. However, in emerging markets, its effectiveness remains debated due to regulatory fragmentation, governance variability, and uneven enforcement mechanisms.

Purpose: This study aims to examine the impact of ESG disclosure on organizational performance within the institutional context of emerging markets.

Methods: This study employed a qualitative design based on document analysis. Data were obtained from the Scopus database using the keyword “ESG Disclosure on Organizational Performance”, limited to open-access publications from 2018 to 2026. A total of 34 documents, consisting of 33 journal articles and 1 institutional report, were analyzed using qualitative content analysis.

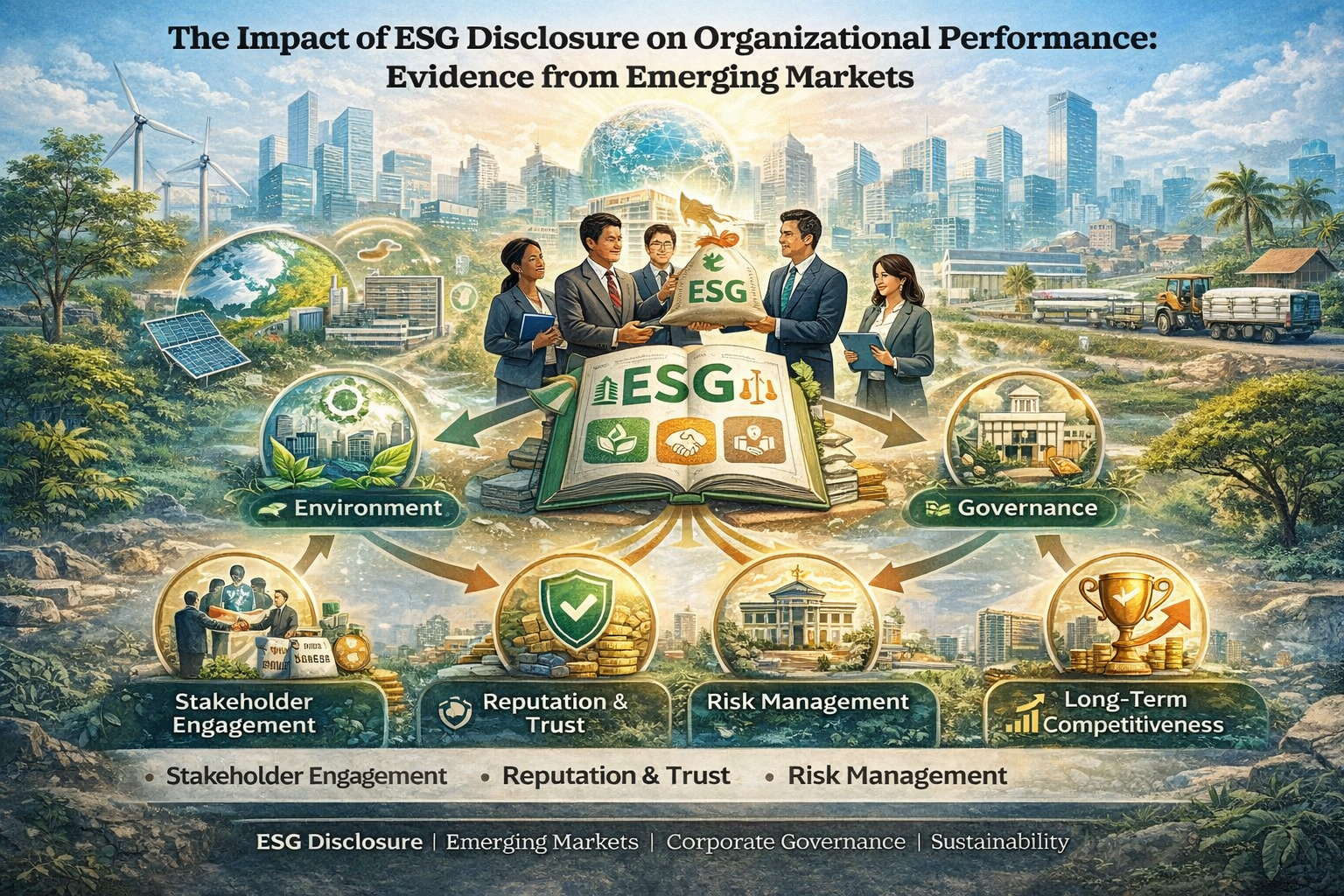

Results: The findings reveal that ESG disclosure functions as a legitimacy-building mechanism that enhances stakeholder engagement, reduces information asymmetry, and strengthens reputational capital. However, the effectiveness of ESG practices depends largely on institutional quality and the maturity of corporate governance systems. The study also shows that ESG disclosure has more meaningful performance implications when ESG principles are integrated into strategic decision-making, risk management, and performance evaluation processes, rather than treated merely as symbolic compliance.

Conclusions: ESG disclosure in emerging markets should not be viewed solely as a reporting requirement, but as a strategic mechanism that can influence organizational legitimacy, stakeholder trust, and long-term competitiveness.

Research Contribution: This study contributes to the ESG-performance literature by providing a qualitative perspective on how institutional constraints shape ESG practices in emerging markets and by emphasizing the strategic role of ESG integration in supporting sustainable organizational performance.

References

Adomako, S., Simms, C., Vazquez‐Brust, D., & Nguyen, H. T. T. (2023). Stakeholder green pressure and new product performance in emerging countries: a cross‐country study. British Journal of Management, 34(1), 299–320.

Al Amosh, H. (2025). Exploring the influence of accounting reporting complexity on ESG disclosure. Corporate Social Responsibility and Environmental Management, 32(5), 5760–5778.

Al-Hiyari, A., Ismail, A. I., Kolsi, M. C., & Kehinde, O. H. (2023). Environmental, social and governance performance (ESG) and firm investment efficiency in emerging markets: the interaction effect of board cultural diversity. Corporate Governance: The International Journal of Business in Society, 23(3), 650–673.

Alhoussari, H. (2025). Integrating ESG criteria in corporate strategies: determinants and implications for performance. Journal of Ecohumanism, 3(8), 2968–2979.

Ali, M. A., & Kamraju, M. (2025). Accountability, transparency, and adaptation strategies. In Global Climate Governance: Strategies for Effective Management (pp. 135–154). Springer.

Aljebrini, A., Dogruyol, K., & Ahmaro, I. Y. Y. (2025). How strategic planning enhances ESG: Evidence from mission statements. Sustainability, 17(2), 595.

Battaglia, M., Ceglia, I., Calabrese, M., & Iandolo, F. (2025). Systemic risk management and stakeholder engagement: insights from business CSR disclosure. Corporate Social Responsibility and Environmental Management, 32(3), 4295–4314.

Boateng, R. N., Tawiah, V., & Tackie, G. (2022). Corporate governance and voluntary disclosures in annual reports: a post-International Financial Reporting Standard adoption evidence from an emerging capital market. International Journal of Accounting & Information Management, 30(2), 252–276.

Carnini Pulino, S., Ciaburri, M., Magnanelli, B. S., & Nasta, L. (2022). Does ESG disclosure influence firm performance? Sustainability, 14(13), 7595.

Chen, S., Song, Y., & Gao, P. (2023). Environmental, social, and governance (ESG) performance and financial outcomes: Analyzing the impact of ESG on financial performance. Journal of Environmental Management, 345, 118829.

Colak, M., & Sarioglu, M. (2025). The Effect of Corporate Governance on the Quality of Integrated Reporting and ESG Risk Ratings. Sustainability, 17(11), 4868.

Cresswell, J. (2016). Research design: Pendekatan metode kualitatif, kuantitatif, dan campuran (Edisi 4). Yogyakarta: Pustaka Pelajar.

De Villiers, C., La Torre, M., & Molinari, M. (2022). The Global Reporting Initiative’s (GRI) past, present and future: critical reflections and a research agenda on sustainability reporting (standard-setting). Pacific Accounting Review, 34(5), 728–747.

Dmuchowski, P., Dmuchowski, W., Baczewska-Dąbrowska, A. H., & Gworek, B. (2023). Environmental, social, and governance (ESG) model; impacts and sustainable investment–Global trends and Poland’s perspective. Journal of Environmental Management, 329, 117023.

Du, S., El Akremi, A., & Jia, M. (2023). Quantitative research on corporate social responsibility: A quest for relevance and rigor in a quickly evolving, turbulent world. Journal of Business Ethics, 187(1), 1–15.

Durmus Senyapar, H. N. (2024). Sustainability marketing strategies for the energy sector: Trends, challenges, and future directions. Environment and Social Psychology, 9(5), 2573.

Ellili, N. O. D. (2022). Impact of ESG disclosure and financial reporting quality on investment efficiency. Corporate Governance: The International Journal of Business in Society, 22(5), 1094–1111.

Hristov, I., Appolloni, A., Cheng, W., & Venditti, M. (2023). Enhancing the strategic alignment between environmental drivers of sustainability and the performance management system in Italian manufacturing firms. International Journal of Productivity and Performance Management, 72(10), 2949–2976.

Iazzi, A., Papa, A., Palladino, R., & Lamusta, S. (2025). Evaluating Companies’ Impression Management Tactics in Mandatory Sustainability Reporting. Business Strategy and the Environment, 34(6), 6828–6848.

Iddrisu, A., Abubakari, M. T., & Tetteh, M. L. (2025). Barriers to Effective ESG Regulation: Lessons from the COVID-19 Crisis. In Financial Regulation, Governance, and Stability (pp. 246–270). Routledge.

Itan, I., Sylvia, S., Septiany, S., & Chen, R. (2025a). The influence of environmental, social, and governance disclosure on market reaction: evidence from emerging markets. Discover Sustainability, 6(1), 347.

Itan, I., Sylvia, S., Septiany, S., & Chen, R. (2025b). The influence of environmental, social, and governance disclosure on market reaction: evidence from emerging markets. Discover Sustainability, 6(1), 347.

Kandpal, V., Jaswal, A., Santibanez Gonzalez, E. D. R., & Agarwal, N. (2024a). Corporate social responsibility (CSR) and ESG reporting: Redefining business in the twenty-first century. In Sustainable energy transition: Circular economy and sustainable financing for environmental, social and governance (ESG) practices (pp. 239–272). Springer.

Kandpal, V., Jaswal, A., Santibanez Gonzalez, E. D. R., & Agarwal, N. (2024b). Corporate social responsibility (CSR) and ESG reporting: Redefining business in the twenty-first century. In Sustainable energy transition: Circular economy and sustainable financing for environmental, social and governance (ESG) practices (pp. 239–272). Springer.

Kauppi, K. (2022). Institutional theory. In Handbook of theories for purchasing, supply chain and management research (pp. 320–334). Edward Elgar Publishing.

Kesar, B. (2025). Impact of social media adoption on stakeholder engagement and trust. Management Matters, 1–29.

Khan, M. A. (2022). ESG disclosure and firm performance: A bibliometric and meta analysis. Research in International Business and Finance, 61, 101668.

Laokulrach, M. (2025). ESG Integration in Investment Analysis. In Environmental, Social, and Governance (ESG) Investment and Reporting (pp. 93–117). Springer.

Malik, N., & Kashiramka, S. (2024). Impact of ESG disclosure on firm performance and cost of debt: Empirical evidence from India. Journal of Cleaner Production, 448, 141582.

Mohammad, W. M. W., Osman, M., & Rani, M. S. A. (2023). Corporate governance and environmental, social, and governance (ESG) disclosure and its effect on the cost of capital in emerging market. Asian Journal of Business Ethics, 12(2), 175–191.

Mukhtar, B., Shad, M. K., Woon, L. F., Haider, M., & Waqas, A. (2024). Integrating ESG disclosure into the relationship between CSR and green organizational culture toward green Innovation. Social Responsibility Journal, 20(2), 288–304.

Nagriwum, T. M., Zhu, N., & Saeed, U. F. (2025). Navigating ESG Performance Through Management Ability, Innovation, and Stakeholder Pressure. A Novel Moderation Analysis. Business Ethics, the Environment & Responsibility.

Noch, M. Y. (2025). Embedding ESG into Strategic Management: Redesigning Corporate Strategy for Sustainable Competitiveness. Journal of Sustainability Industrial Engineering and Management System, 4(1), 336–350.

Ridwan, M., & Alghifari, E. S. (2025). Evaluating the impact of ESG on financial risk: the moderating effects of operational ability and profitability in Indonesian infrastructure firms. Journal of Accounting & Organizational Change, 21(6), 992–1015.

Singhania, M., & Saini, N. (2023a). Institutional framework of ESG disclosures: comparative analysis of developed and developing countries. Journal of Sustainable Finance & Investment, 13(1), 516–559.

Singhania, M., & Saini, N. (2023b). Institutional framework of ESG disclosures: comparative analysis of developed and developing countries. Journal of Sustainable Finance & Investment, 13(1), 516–559.

Sugianto, N. A. P., Riandy, C. N., Zainavy, S. F., & Hartikasari, A. I. (2022). The contribution of Environmental, Social, and Governance (ESG) disclosure to reduce investor asymmetry information. Proceedings Series on Social Sciences & Humanities, 7, 56–61.

Volpone, S. D., Casper, W. J., Wayne, J. H., & White, M. L. (2025). Are Employees Committed to Diversity at Work and in Their Personal Lives? The Role of Organizational Antiracist Signaling Following a Racial Injustice Event. Human Resource Management, 64(5), 1401–1420.

Wang, J. (2026). ESG, Cost of Capital, and Access to Financing. In ESG Strategies and Financial Markets: Antecedents, Corporate Decision-Making, and Real Effects (pp. 151–178). Springer.

Wiredu, I., Zhu, N., Agyemang, A. O., & Borgi, H. (2025). Driving circular economy strategies for sustainable development: The role of board capital and innovation capacity in emerging markets. Business Strategy and the Environment, 34(5), 5544–5562.

Wong, W.-K., Teh, B.-H., & Tan, S.-H. (2023a). The influence of external stakeholders on environmental, social, and governance (ESG) reporting: Toward a conceptual framework for ESG disclosure. Foresight and STI Governance, 17(2), 9–20.

Wong, W.-K., Teh, B.-H., & Tan, S.-H. (2023b). The influence of external stakeholders on environmental, social, and governance (ESG) reporting: Toward a conceptual framework for ESG disclosure. Foresight and STI Governance, 17(2), 9–20.

Wong, W.-K., Teh, B.-H., & Tan, S.-H. (2023c). The influence of external stakeholders on environmental, social, and governance (ESG) reporting: Toward a conceptual framework for ESG disclosure. Foresight and STI Governance, 17(2), 9–20.

Wong, W.-K., Teh, B.-H., & Tan, S.-H. (2023d). The influence of external stakeholders on environmental, social, and governance (ESG) reporting: Toward a conceptual framework for ESG disclosure. Foresight and STI Governance, 17(2), 9–20.

Yahaya, O. A. (2026). Does ESG performance reduce the cost of capital in Nigeria. Journal of Accounting and Finance Research, 14(2), 144–177.

Downloads

Published

Data Availability Statement

Data sharing is not applicable to this article because no new data were created or analyzed in this study.

Issue

Section

License

Copyright (c) 2026 Neng Nur Annisa, Maria Margarita R. Lavides (Author)

This work is licensed under a Creative Commons Attribution-ShareAlike 4.0 International License.

Copyright

Authors who publish with this journal agree to the following terms:

- Authors retain copyright and grant the journal right of first publication with the work simultaneously licensed under a Creative Commons Attribution-ShareAlike 4.0 International License that allows others to share the work with an acknowledgment of the work's authorship and initial publication in this journal.

- Authors are able to enter into separate, additional contractual arrangements for the non-exclusive distribution of the journal's published version of the work (e.g., post it to an institutional repository or publish it in a book), with an acknowledgment of its initial publication in this journal.

- Authors are permitted and encouraged to post their work online (e.g., in institutional repositories or on their website) prior to and during the submission process, as it can lead to productive exchanges, as well as earlier and greater citation of published work (See The Effect of Open Access).

License

This work is licensed under a Creative Commons Attribution-ShareAlike 4.0 International License.

You are free to:

- Share — copy and redistribute the material in any medium or format for any purpose, even commercially.

- Adapt — remix, transform, and build upon the material for any purpose, even commercially.

- The licensor cannot revoke these freedoms as long as you follow the license terms.

Under the following terms:

- Attribution — You must give appropriate credit , provide a link to the license, and indicate if changes were made . You may do so in any reasonable manner, but not in any way that suggests the licensor endorses you or your use.

- ShareAlike — If you remix, transform, or build upon the material, you must distribute your contributions under the same license as the original.

- No additional restrictions — You may not apply legal terms or technological measures that legally restrict others from doing anything the license permits.

Notices:

You do not have to comply with the license for elements of the material in the public domain or where your use is permitted by an applicable exception or limitation .

No warranties are given. The license may not give you all of the permissions necessary for your intended use. For example, other rights such as publicity, privacy, or moral rights may limit how you use the material.